1

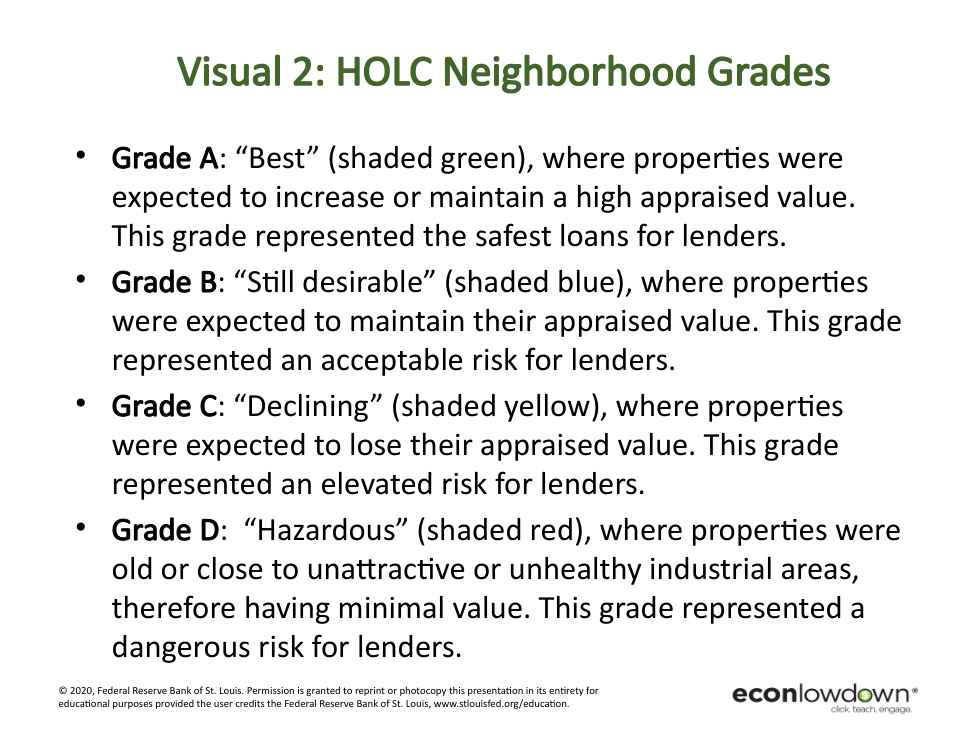

Describe the details of the image in complete sentences.

Describe the details of the image in complete sentences.

0

What is the message that the image is communicating?

What is the message that the image is communicating?

Week long lesson investigating the history and concequences of redlining practices in by real estate agents and banks in America after the New Deal.

JU.6-8.12 : I can recognize and describe unfairness and injustice in many forms including attitudes, speech, behaviors, practices and laws.

SS.EC.1.6-8.LC. Explain how economic decisions affect the well-being of individuals, businesses and society.

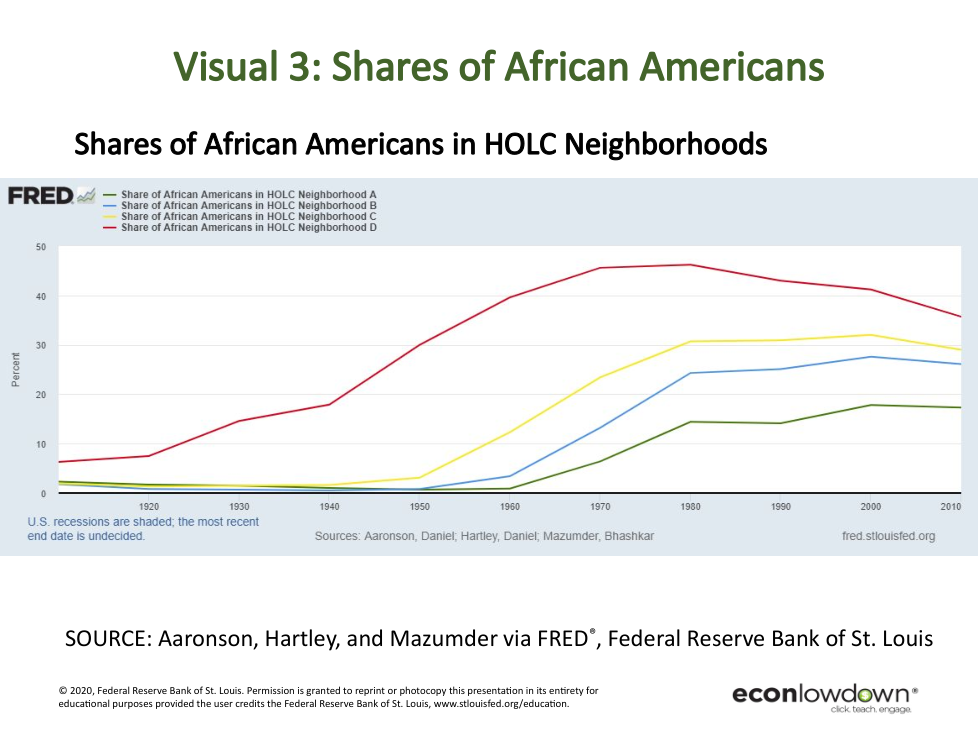

Describe the details of the image in complete sentences.

What is the message that the image is communicating?

What event took place in Tiananmen Square in 1989?

What was the main demand of the protesters in Tiananmen Square?

How did the Chinese government respond to the protests in Tiananmen Square?

What was the outcome of the Tiananmen Square protests?

Title: Understanding Injustice: Unfairness Beyond the Surface Injustice is a concept that many of us are familiar with, but what does it really mean? In simple terms, injustice refers to any act or situation that goes against fairness or equality. It occurs when people are treated unfairly or denied the rights they deserve. Understanding injustice is crucial in making our world a more equitable place. One clear example of injustice is discrimination. Discrimination happens when someone is treated differently because of their race, gender, religion, or any other characteristic. For instance, if a person is not hired for a job solely based on their gender or ethnicity, it is considered unjust. Another form of injustice is social inequality. This occurs when certain groups in society have less access to resources and opportunities compared to others. For example, when some children do not have access to quality education because of their socioeconomic background, it is an example of social inequality. Injustice can also manifest through systemic issues. These are deeply ingrained problems in society that perpetuate unfairness. For example, when the legal system disproportionately targets and punishes individuals from specific communities, it is a manifestation of systemic injustice. Recognizing injustice is the first step towards fighting against it. To create a fairer society, it is important to educate ourselves and others about these issues, promote empathy and understanding, and advocate for change. By working together, we can combat injustice and build a more equitable future for all.

What is injustice?

How comfortable do you feel intervening when you experience someone treating someone unfairly or with prejudice?

What do you think it is that makes you comfortable or uncomfortable in these situations?

Title: Redlining Practices in 1940's Chicago Introduction In the 1940's, the city of Chicago experienced a discriminatory practice known as redlining. This unfair practice negatively impacted communities based on their racial makeup. Redlining prevented people of color, particularly African Americans, from accessing loans, buying houses, and ultimately building wealth. Let's delve into the details of redlining and its effects on Chicago during this time. What is redlining? Redlining is a system where lending institutions draw maps and label certain neighborhoods as risky or undesirable for loans. These neighborhoods were usually populated by minority groups, notably African Americans. This discriminatory system made it difficult for those living in these neighborhoods to secure loans for homes and businesses. Effects on Chicago The effects of redlining in Chicago were devastating. African Americans were confined to certain neighborhoods, mainly the South Side and the West Side, and had limited opportunities for economic growth. These areas became overcrowded, with dilapidated housing, low-quality schools, and limited access to quality healthcare and other essential services. Long-lasting consequences The legacy of redlining continues to affect Chicago to this day. Limited access to loans and opportunities resulted in a growing wealth gap between white and minority communities. Discrimination in housing perpetuated segregation and hindered social and economic progress for African Americans. Conclusion Understanding the redlining practices in 1940's Chicago helps us recognize the systemic barriers faced by minority communities and their ongoing impact. By acknowledging this historical injustice, we can work towards creating a more equitable society where all individuals have equal opportunities to thrive.

What was the impact of redlining?

What did "redlining " specifically do?

What is the main effect of redlining on Chicago?

Redlining refers to:

Redlining is an example of:

Redlining disproportionately affected:

The practice of redlining was primarily used to:

Select all choices below that are true about loans.

Drag each of the following actions below into the correct category.

Only being shown homes in specific neighborhoods based on your race.

Being denied a loan because of your race

Applying for a loan

Buying a home on the south side of Chicago

Being charged a higher interest rate for a bank loan based on the neighborhood you are buying a home in.

Act of Redlining

Not an act of Redlining

Select all of the following statements that are false based on the chart to the left.

Based on the map is invested in LatinX communities in Chicago.

Based on the map is invested in Black communities in Chicago.

Based on the map is invested in The South Side communities in Chicago.

Interactive maps of redlining around the U.S. from 1940.

https://dsl.richmond.edu/panorama/redlining/#loc=5/39.1/-94.58

Working with one partner. Choose a city on the interactive map. click on a redlined area and read the original notes about that area.

What city did you choose?

What part of the city is the redline neighborhood that you chose in?

What is the racial breakdown of the neighborhood?

What are key components of how they describe the neighborhood?

Be ready to report the key details on chart paper for the rest of the class.

Research the area that you chose from the redline map, and compare the conditions of that area in the past to the conditions at present.

Record your notes and findings here.

Be ready to report all findings to the rest of the group on chart paper.

https://interactive.wbez.org/2020/banking/disparity/

What data was used in the article to explain the negative effects of redlining in Chicago?

Copy and paste a quote from the article to support your answer.

https://revealnews.org/article/for-people-of-color-banks-are-shutting-the-door-to-homeownership/

by Aaron Glantz and Emmanuel MartinezFebruary 15, 2018

Fifty years after the federal Fair Housing Act banned racial discrimination in lending, African Americans and Latinos continue to be routinely denied conventional mortgage loans at rates far higher than their white counterparts.

What are some of the reasons that banks use to explain why they do not lend money in black neighborhoods?

Copy and paste a quote from the above article to support your answer.

What is one clear example of injustice?

What does social inequality refer to?

Based on what is presented in the video thus far, What does a Sponsor do? Why are Sponsors neccessary?

In the conversation they women use the terms, "illegal" and "Undocumented" to describe the little girl.

1) What is the difference between the two terms?

The mans says, " I appreciate what you are doing, I just don't know why it has to be here."

The man could have meant Texas or the U.S. as a whole in this statement. What would your answer be to the man in either case?

The woman says, "They have a system, right or wrong" then goes on to say, "It may not be working but that is the system."

1) Why do you think the woman feels comfortable with a system that she seems to admit is not working?

2) What could be potentially problematic about this type of thinking when we consider other issues in the country?

What information does the Man offer that represents the strongest support for his arguement?

Which level of oppression is occurring in this video?

What is a loan?

Which of the following will likely be included in a loan application

Loan to buy a house

Loan to start a business

Loan book a trip

Loan to pay for college

Loan to buy groceries before next paycheck

Collateral Loan / secured loan

Non Collateral Loan / unsecured loan

When was the great Depression? What caused the Great Depression?

Which two programs were created

If White people applied for a loan, the Federal Housing Administration would guarantee to pay the loan back to the bank, even if the White applicants could not pay the loan back.

If Black people applied for a loan, the Federal Housing Administration would guarantee to pay the loan back to the bank, even if the Black applicants could not pay the loan back.

What does he mean by, "Black neighborhoods were off limits to banks?"

What is 3.9% of 500,000?

What is 6.9% of 125,000?

This map shows a very large amount of arrests for drug possession in Black communities of Baltimore and very few in the White communities of Baltimore. The research shows that Black people and White people use drugs at an equal rate. If police were being intentionally racist in their practices, why might it be easy to arrest black people?

Which areas of life did redlining have the strongest impact on for people in Black and Brown communities?

Working with one partner. Choose a city on the interactive map. click on a greenlined area and read the original notes about that area.

What city did you choose?

What part of the city is the redline neighborhood that you chose in?

What is the racial breakdown of the neighborhood?

What are key components of how they describe the neighborhood?

Be ready to report the key details on chart paper for the rest of the class.

Research the area that you chose from the green-lined map, and compare the conditions of that area in the past to the conditions at present.

Record your notes and findings here.

Be ready to report all findings to the rest of the group on chart paper.

The Federal Housing Administration program guaranteed banks would receive payment for loans that they made even if the person never paid them back.

The FHA program was only available to banks that loaned money to white people.