READ THIS!

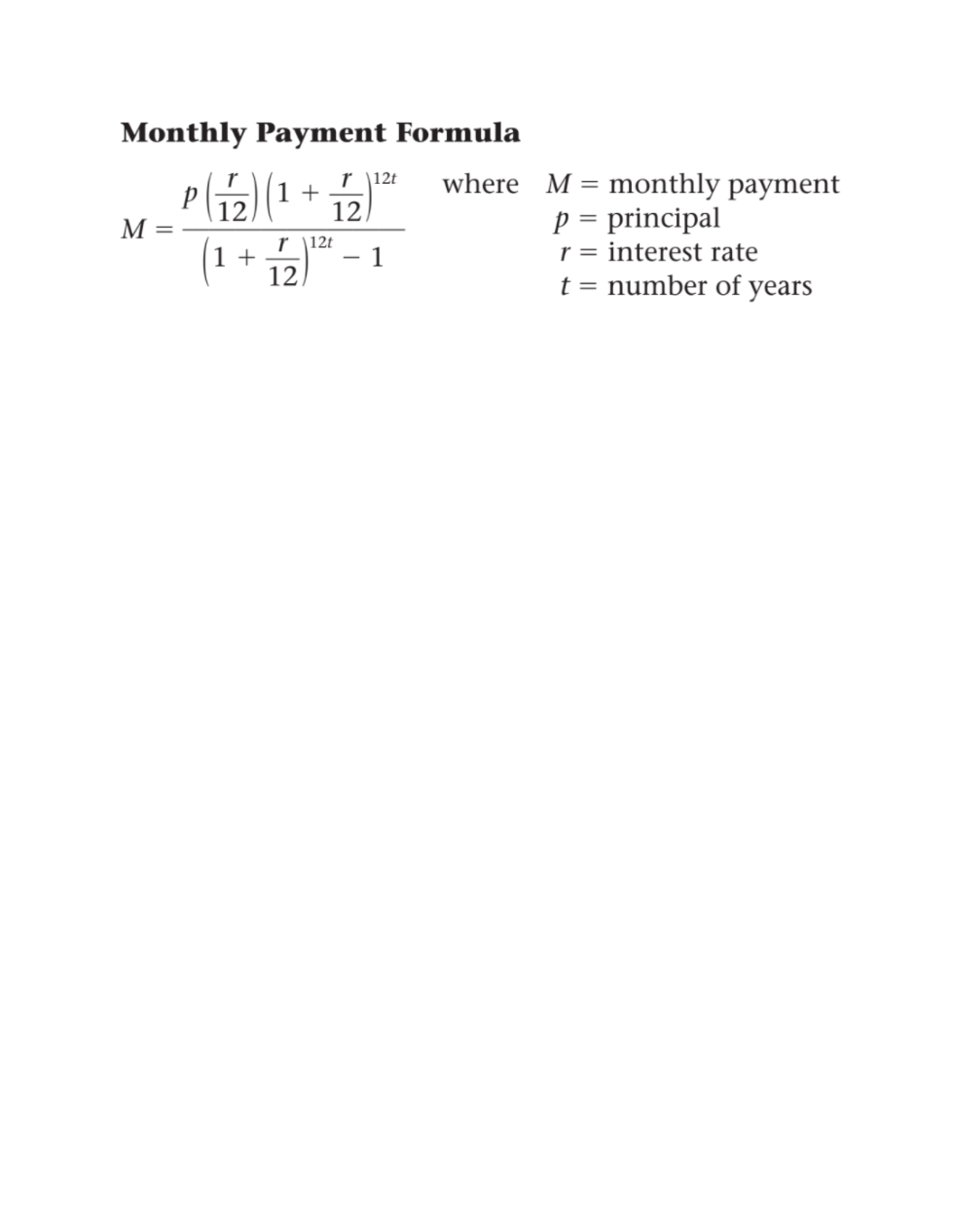

The past few lessons we have used the Monthly Payment Formula to calculate how much someone would have to pay back each month when taking out a loan.

This formula incorporates both the principal and interest that the consumer would pay back each month.

Because of high interst rates, it can be really expensive to borrow money!

But don't fear!

We can bring down our monthly loan payments by first applying a down payment.

A down payment is a one time payment that will ultimetly lower how much you have to borrow and thus lower your interest owed.

The higher your down payment, the lower the monthly payments will be!