Micro 2.7-Maximum and Minimum Price Controls

star

star

star

star

star

Last updated 11 months ago

8 Nsɛmmisa

Prices send signals and provide incentives to buyers and sellers. When supply or demand changes, market prices adjust, affecting incentives. High prices induce extra production while they discourage consumption. In this exercise, we discover how the imposition of price controls (maximum or minimum prices) interrupts the process that matches production with consumption. Price ceilings (maximum prices) sometimes appear in the form of rent control, utility prices and other caps on upward price pressure.

Price floors (minimum prices) also occur in the form of prevailing wages and minimum wages.

When government imposes price controls, citizens should understand that some people gain and some people lose from every policy change. By understanding the consequences of legal price regulations, citizens are able to weigh the costs and benefits of the change. As a general rule, price floors create a surplus of goods or services, or excess supply, since the quantity demanded of goods is less than the quantity supplied. Conversely, price ceilings generate excess quantity demanded, causing shortages.

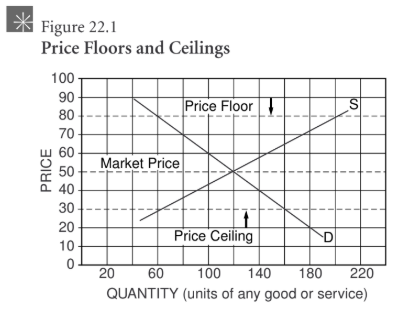

What is the market price?

What quantity is demanded and what quantity is supplied at the market price?

What quantity is demanded if the government passes a law requiring the price to be no higher than $30? This is called a price ceiling.

What quantity is supplied if the government passes a law requiring the price to be no higher than $30? This is called a price ceiling.

If the government imposes a price ceiling of $30, there will be a of units since .

What quantity is demanded if the government passes a law requiring the price to be no lower than $80? This is called a price floor.

What quantity is supplied if the government passes a law requiring the price to be no lower than $80? This is called a price floor.

If the government imposes a price floor of $80, there will be a of units since the .